Federal Budget 2026–27

What was announced — and what it actually means for you.

The Federal Budget delivered by Treasurer Jim Chalmers on Tuesday 12 May 2026 includes significant changes to tax, property and investment rules. While some measures have attracted strong public commentary, most changes are phased in gradually and include important grandfathering and transition arrangements.

On Budget night we sent clients a short summary of the headline measures. This piece expands on that — with the detail, the context, and our view of what it actually means for the families and business owners we work with.

In this update

Capital gains tax (CGT) changes and grandfathering

- Property and negative gearing

- Superannuation — what’s unchanged

- Family trust taxation and transition rules

- Impacts on small business and complex structures

- Portfolio and asset allocation considerations

- Start-ups and high-growth business concerns

- Budget Q&A and next steps

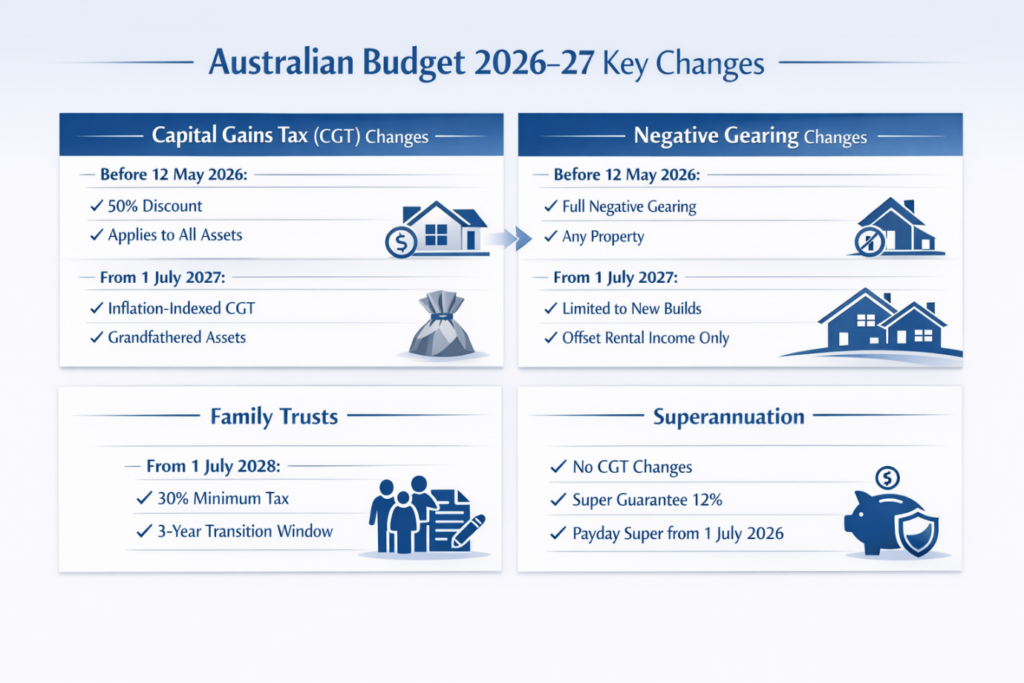

Capital gains tax (CGT) — what’s changing

From 1 July 2027, the Government will replace the long-standing 50% CGT discount for individuals and trusts with a new system that taxes real gains (after inflation) rather than nominal gains. The new system will tax real (after-inflation) gains at a minimum effective rate of 30 per cent.

Key points

- Assets owned before 7:30pm (AEST) on 12 May 2026 are grandfathered.

- Capital growth earned before 1 July 2026 retains its existing CGT treatment.

- The new rules apply only to capital growth earned after that date.

- Assets are not required to be re-valued at 30 June 2026.

When an asset is sold, the overall gain is expected to be apportioned over time, with:

- Pre-reform growth taxed under the old rules (including the 50% discount where it currently applies); and

- Post-reform growth taxed under the new inflation-indexed rules.

The family home (main residence) is not affected. Investors in newly built residential housing will be able to choose between the existing 50% CGT discount and the new arrangements.

The takeaway: this is a meaningful change, but it operates prospectively. Gains accrued on assets you already own keep their existing treatment. There is no need to crystallise gains in panic.

Property and negative gearing

Existing property investments

- Residential investment properties purchased before Budget night retain full negative gearing.

- This treatment continues until the property is sold.

New property purchases

- From 1 July 2027, negative gearing will be limited to new-build residential property.

- Losses on established properties will generally be limited to offsetting:

- Rental income; or

- Capital gains (rather than employment income).

The policy is intended to encourage new housing supply, rather than remove tax deductions from existing investors. For clients with existing portfolios, the practical effect is that the tax characteristics of those properties are locked in; future decisions about additional property investment will need to be modelled under the new rules.

Superannuation — largely unchanged

Despite considerable pre-Budget speculation, superannuation was not materially affected by the main tax reform measures:

- The CGT changes do not apply to super funds.

- Existing super CGT concessions remain unchanged.

- The Superannuation Guarantee is locked at 12%.

- Payday super begins from 1 July 2026, aligning super payments with wage payments.

Super continues to be one of the most concessionally taxed long-term investment structures in Australia — and arguably more attractive in relative terms after this Budget, given that investment income outside super is now taxed more heavily.

Changes to tax on family (discretionary) trusts

From 1 July 2028, the Budget introduces a minimum 30 per cent tax rate on distributions from discretionary (family) trusts.

Important clarifications

- The tax is levied at the trustee level, not the beneficiary level.

- It does not apply to fixed trusts, superannuation funds, deceased estates or charitable trusts.

- The measure is aimed at reducing income-splitting advantages over time.

This change is particularly relevant for

- Small business owners operating through family trusts.

- Higher-wealth individuals using trusts as long-term holding vehicles.

- Investment structures involving multiple family members or related entities.

Transition period and restructuring flexibility

Recognising the complexity of trust structures, the Government has provided a three-year transition period:

- From 1 July 2027 to 30 June 2030.

- During this period, eligible trusts can:

- Restructure into companies or fixed trusts.

- Access rollover relief (subject to final legislation).

This transition window is intended to allow enough time to:

- Review structures.

- Model tax outcomes.

- Restructure where appropriate without forcing immediate decisions.

No action is required immediately, but forward planning is important for affected clients.

What this means for small business and complex structures

For clients with more sophisticated arrangements — operating businesses, multiple entities, family trusts and investment assets held alongside personal holdings — the Budget increases the importance of getting the architecture right. Three areas in particular:

- Entity selection. The relative tax efficiency of companies, fixed trusts and discretionary trusts shifts under the new rules. Structures that made sense five years ago may not be optimal five years from now.

- Asset location. Where each asset sits — personal names, super, companies or trusts — becomes more consequential as the tax characteristics of each wrapper diverge.

- Profit distribution strategies. Distribution patterns that rely heavily on income splitting through discretionary trusts will be less effective over time.

Structures established primarily for income splitting may be less effective from 2028 onwards. Structures established for legitimate asset protection, succession or operational reasons remain entirely viable, but should be reviewed with fresh eyes.

The impact on investments and portfolios

These Budget changes narrow the tax difference between income (like interest, dividends and rent) and capital gains. That means portfolio decisions can be guided more by investment fundamentals, your goals and time horizon, and less by tax timing (such as holding an asset just past 12 months to receive the discount).

In practical terms, this may mean

- For investments made from 1 July 2026, there is no extra tax benefit from holding an asset beyond 12 months purely to access a CGT discount.

- Income-producing investments (dividends, distributions and rental yield) may become relatively more attractive after tax.

- Capital growth still matters, but the focus shifts toward real (after-inflation) growth and the investment’s role in your portfolio.

- When deciding whether to sell, tax becomes a significantly smaller part of the investment decision, with greater emphasis on investment fundamentals, valuation, diversification and risk.

- Overall, portfolio construction may place more weight on total return, reliable income and diversification — aligned to your income needs, volatility tolerance and time horizon — with tax implications being less of a factor when selecting investments.

Start-ups and high-growth businesses

One area of genuine concern arising from this Budget is the potential impact on start-ups and high-growth businesses — particularly those that rely on equity to attract founders, investors and senior talent. By reducing the long-term tax concession on capital gains for new investments, Australia risks becoming less competitive relative to other jurisdictions that offer more favourable tax outcomes for successful business exits.

For founders and early employees, who often accept lower cash remuneration in exchange for equity upside, the after-tax reward for building and exiting a business is an important consideration. If those rewards are materially reduced, it increases the likelihood that some start-ups may choose to establish holding companies, intellectual property or even entire corporate structures offshore — even if the underlying operations remain in Australia.

While the Government has indicated it wants to continue supporting productive investment and innovation, and further detail may emerge through legislation or consultation, there is a risk that without targeted relief these changes could unintentionally discourage high-growth entrepreneurial activity or divert it overseas over time. We will continue to monitor how these rules are refined and what they mean for founders, investors and employees holding equity-based interests.

Budget Q&A — common questions

Do I need to value my assets at 30 June 2026?

No. The CGT changes do not require assets to be re-valued. Tax is calculated when an asset is sold, using a time-based apportionment of gains.

Will I lose tax benefits I’ve already earned?

No. Existing assets are grandfathered. Tax treatment already accrued is preserved.

Are trusts being abolished or banned?

No. Discretionary trusts can continue to operate. From 1 July 2028, distributions from them may be subject to a minimum 30 per cent tax rate at the trustee level.

Should I sell property or investments before the rules change?

In most cases, there is no urgent need to act. Decisions should be based on personal circumstances — your goals, cash flow, time horizon and overall plan — rather than headlines.

What should you do now?

For most clients:

- No immediate action is required.

- The changes are prospective, phased and include transition periods.

However, if you are:

- Considering selling property or major investments

- Operating through a family trust

- Running a business with multiple entities

- Planning retirement or succession in the next few years

…it may be appropriate to review how these measures interact with your plans. That review is unlikely to require any drastic action this year, but the work is worth doing now rather than closer to the 2027 and 2028 commencement dates.

If you’d like to talk through how any of this lands on your own situation, that’s exactly the conversation we welcome.

General Advice Warning

The information in this article is general in nature and has been prepared without taking into account your personal objectives, financial situation or needs. It does not constitute personal financial, tax or legal advice. The Federal Budget measures described above are based on announcements made on 12 May 2026 and may be subject to change as legislation is drafted, debated and passed through Parliament. Specific tax outcomes depend on individual circumstances and the final form of any enacted legislation. Before acting on any of the information, you should consider its appropriateness having regard to your own objectives, financial situation and needs, and seek professional advice from a qualified financial adviser, accountant or lawyer. Ora Private Wealth and its representatives do not accept liability for any loss or damage arising from reliance on the information contained in this article.